Solar Is the Future, But What Does That Mean for Suzlon Energy and Inox Wind?

Alex Smith

1 hour ago

Synopsis: Solar is racing ahead and could reshape India’s renewable energy market. But the rise of cheap solar and batteries may also decide the future of Suzlon Energy and Inox Wind. Can these two wind giants survive the solar boom?

India’s renewable-energy transition is increasingly being led by solar power. Solar projects are faster to install, tariffs are low and capacity can be developed across utility-scale parks, factories, farms and rooftops. Waaree Energies latest earnings presentation shows the estimates that India’s installed solar capacity could rise from 102 GW in FY25 to 341 GW by FY30, with annual additions reaching 45 GW in FY27 and 50 GW in each of the following three years.

This appears worrying for wind-turbine manufacturers. If solar remains the cheapest source of new electricity and batteries become cheaper, investors may wonder whether India will still need large wind additions. However, electricity demand does not end when sunlight disappears.

The future of Suzlon Energy and Inox Wind will depend on whether wind remains an economical part of round-the-clock renewable power and whether both companies can convert that opportunity into cash flows.

Why Solar Is Clearly Winning The Capacity Race

Waaree expects solar tariffs to remain near Rs. 2.5/kWh and describes solar as the cheapest new source of electricity. Policy support, domestic manufacturing, rooftop installations and commercial demand are expected to keep the sector growing. Its forecast of around 45-50 GW of annual solar additions is several times larger than the wind industry’s current installation level.

{kind=link}

Source: Suzlon Energy Q4FY26 Earnings Call Transcript

Solar can be built in more locations and can serve different markets. Wind projects depend on suitable wind resources, large land parcels, transport infrastructure and grid connectivity at specific sites. Solar will therefore probably remain the main driver of renewable capacity additions.

However, adding solar creates another problem. Much of the capacity produces electricity during the same daytime hours. As penetration increases, the system can face surplus generation and curtailment while still needing power during the evening and night. Waaree expects India to require 232 GWh of storage by 2032 to reduce curtailment and support grid stability. The real question is not whether solar wins, but how India will supply renewable electricity when consumers need it.

Why More Solar Does Not Make Wind Redundant

Waaree calls solar the fastest, cheapest and easiest source of energy, but also acknowledges that it goes out with the sun while the grid needs electricity throughout the day. Batteries can store daytime power and release it later, but they store electricity rather than generate it.

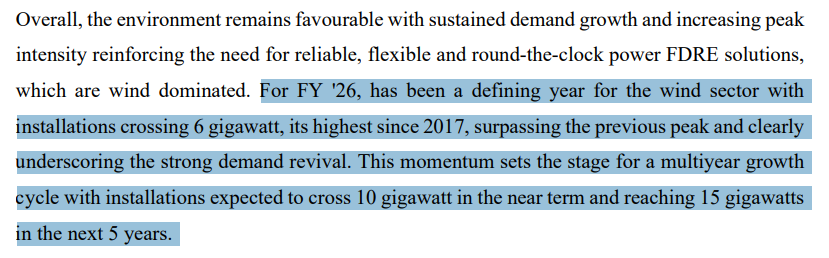

Inox Wind management argues that 16-hour battery storage is still not financially viable. It believes wind remains important because it generates during non-solar hours, helps balance the grid and improves transmission utilisation. Management expects Indian wind additions to rise from a record 6 GW in FY26 to around 8-10 GW annually, supported by round-the-clock, firm and dispatchable renewable energy and hybrid projects.

{kind=link}

Source: Inox Wind Q1FY26 Earnings Call Transcript

Suzlon supports the argument with the generation profile. During a recent daytime peak of 270 GW, solar contributed 22 percent and wind 5 percent. During an evening peak of around 250 GW, solar contributed nothing while wind supplied 21 percent, according to management. Suzlon also estimates wind tariffs at around Rs. 3.6-Rs. 3.9 per unit and argues that solar plus storage cannot replace wind unless battery costs fall below roughly Rs. 1.2 per unit.

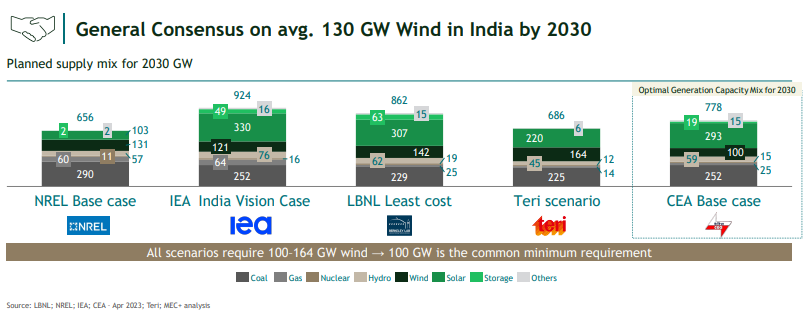

Wind does not need to beat solar during sunny hours. Its value comes from improving the supply profile and reducing storage and grid requirements. Suzlon estimates that India may need more than 130 GW of wind by 2030 to meet non-solar peak demand.

{kind=link}

Source: Suzlon Energy Q4FY26 Investor Presentation

What The Shift Means For Suzlon Energy

Suzlon enters this transition with greater scale. It ended FY26 with a 5.9 GW order book, including 51 percent from commercial, industrial and captive customers, 34 percent from central and state auctions and 15 percent from PSUs. FY26 deliveries reached 2,456 MW, while manufacturing capacity stood at 4.5 GW. It also managed more than 15.7 GW through its operations and maintenance business, with machine availability above 95 percent.

FY26 revenue rose 54 percent to Rs. 16,679 crore, while EBITDA increased 63 percent to Rs. 3,022 crore. PAT of Rs. 3,153 crore included deferred-tax-asset recognition of Rs. 742 crore, which should be separated while assessing underlying profitability.

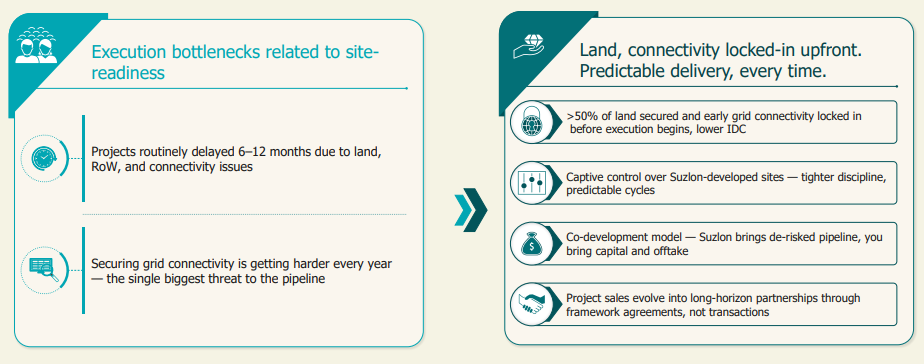

Suzlon is responding to execution problems by increasing its role in project development and EPC. EPC’s share in the order book rose from 20 percent to 28 percent, and management targets 50 percent by FY28. The company is also trying to secure land and connectivity before construction begins. This could give Suzlon greater control over commissioning, but may require more working capital.

{kind=link}

Source: Suzlon Energy Q4FY26 Investor Presentation

The need for control is visible in the numbers. Out of the 2,456 MW delivered in FY26, only 744 MW had been commissioned, while 971 MW had been erected but not installed and another 350 MW was ready for commissioning. Land, right-of-way and grid connectivity can delay projects even after turbines are manufactured. Orders create value only when projects become operational.

What The Shift Means For Inox Wind

Inox Wind ended FY26 with a 3.1 GW order book, providing more than 24 months of visibility. Its mix included 58 percent from auctions, 36 percent from commercial and industrial customers and 6 percent from PSUs. The company won around 600 MW of fresh orders and had an order pipeline exceeding 2 GW.

Its main advantage is the wider INOXGFL ecosystem. Inox Clean plans to add more than 3 GW of renewable capacity annually, with 20-30 percent expected to come from wind. This could provide recurring orders equal to nearly one-third of Inox Wind’s annual execution target. Inox Green can earn O&M income from the resulting assets, while Inox Renewable Solutions can participate in EPC and evacuation infrastructure.

Unlike Suzlon, Inox Wind is reducing exposure to full turnkey EPC. It plans to increase equipment-supply orders to around 75 percent because land costs, right-of-way expenses and delayed payments can block capital in turnkey projects. It will continue selected EPC work, particularly for Inox Clean. This could improve receivables, but leaves more execution responsibility with customers.

Inox Wind is also preparing a 4.4 MW turbine, which management expects to launch during 2026 and use to improve market reach and margins. FY26 total income rose 23 percent to Rs. 4,569 crore and EBITDA reached Rs. 1,232 crore. However, on-ground disruption, logistics issues and delayed customer payments kept working capital high.

Where The Two Strategies Differ

Suzlon is taking more control of development and EPC to reduce site-readiness delays. Inox Wind is moving towards equipment supply to reduce working-capital pressure. Suzlon’s demand is spread across commercial and industrial customers, auctions and PSUs, while Inox expects a meaningful share of future orders from group companies.

Suzlon therefore offers broader direct exposure to an industry-wide recovery in wind installations. Inox Wind offers an integrated model, where solar growth can create turbine, EPC and O&M opportunities across the group. However, this depends on Inox Clean meeting its capacity targets and retaining wind at 20-30 percent of its renewable mix.

The difference changes their risks. Suzlon may gain greater project control but face higher capital needs as EPC expands. Inox Wind may improve cash conversion through equipment supply but remain exposed to delays at customer-controlled sites.

What Could Go Wrong?

The biggest long-term risk is that battery costs fall enough to make long-duration solar storage much cheaper. Waaree is planning a 20 GWh BESS facility, showing that solar companies expect storage to become a major part of the power system. Cheaper storage may not remove wind completely, but it could reduce the wind capacity required for some supply profiles.

The nearer risk is execution. Suzlon must convert its 5.9 GW order book into commissioned capacity without allowing EPC expansion to stretch working capital. Inox Wind must prove that recurring group orders can offset modest FY26 order wins and that equipment supply improves cash conversion. Motilal Oswal highlighted fresh orders, deliveries and working capital as key monitorables for Suzlon, while it cut Inox Wind’s FY27 and FY28 EBITDA estimates.

Solar is likely to remain the largest part of India’s renewable build-out. But a solar-heavy grid will still need power after sunset, better transmission utilisation and firm supply. This gives Suzlon and Inox Wind a future, although not a guaranteed one. Wind must prove its value inside hybrid systems, and both companies must prove that strong industry demand can become profitable, cash-generating execution.

Disclaimer: The views and investment tips expressed by investment experts/broking houses/rating agencies on tradebrains.in are their own, and not that of the website or its management. Investing in equities poses a risk of financial losses. Investors must therefore exercise due caution while investing or trading in stocks. Trade Brains Technologies Private Limited or the author are not liable for any losses caused as a result of the decision based on this article. Please consult your investment advisor before investing.

The post Solar Is the Future, But What Does That Mean for Suzlon Energy and Inox Wind? appeared first on Trade Brains.

Related Articles

Caliber Mining IPO: From Issue Details to Financials; Here’s What You Need to Know

Synopsis: Caliber Mining & Logistics Limited’s ₹450 crore IPO opens on...

Vijay Kedia Buys Fresh 1.45% Stake in This Engineering Stock; Do You Own It?

Synopsis: A well-known name in Dalit Street’s investor circles has picked...

65% Rally in a Year: Engineering Stock Sees Rising FII and DII Stakes, Is Another Rally Ahead?

Synopsis: Institutional investors have been raising their stake steadily even as...

2 Stocks Dominating India’s Mutual Fund RTA Duopoly; Which One Should Investors Pick?

Synopsis: India’s mutual fund industry keeps setting fresh records, and tw...